- Random Words: The Investing Unscripted Newsletter

- Posts

- Finding Your Own Inner Misfit

Finding Your Own Inner Misfit

Jason is more Misfit than Jeff (you can tell by the hair and the returns).

We need your feedback!

In an effort to help more people find the show and to help us balance our work/podcast lives, we’re considering publishing the podcast on a weekday rather than Saturday. But we want to hear from you about this.

Please take a moment to complete this short poll about when you listen to podcasts. Thanks for your help!

Now, onto our random words.

Jeff’s Random Words

I hope by now you’ve had a chance to listen to this week’s episode with Tyler Crowe about his investing newsletter, Misfit Alpha (Tyler is offering Investing Unscripted listeners a 20% discount). I found the conversation especially interesting because the market has felt expensive to me lately. What I mean by that is I’ve been less excited to add to my positions, or even add new ones, because many of the companies I have the highest conviction in right now are not looking like a bargain. And I prefer a bargain.

One of the main points in our conversation with Tyler was that the kinds of companies he’s interested in are typically not expensive. This isn’t because they’re not good businesses but because investors don’t know about them. Remember that in the short term, the stock market is a voting machine.

During 2020 and 2021, many stocks got “voted” up to ridiculous valuations. New (me) or less savvy (also me?) investors ended up buying stocks at valuations that will be very difficult to profit from. Here’s a quick example from my personal life.

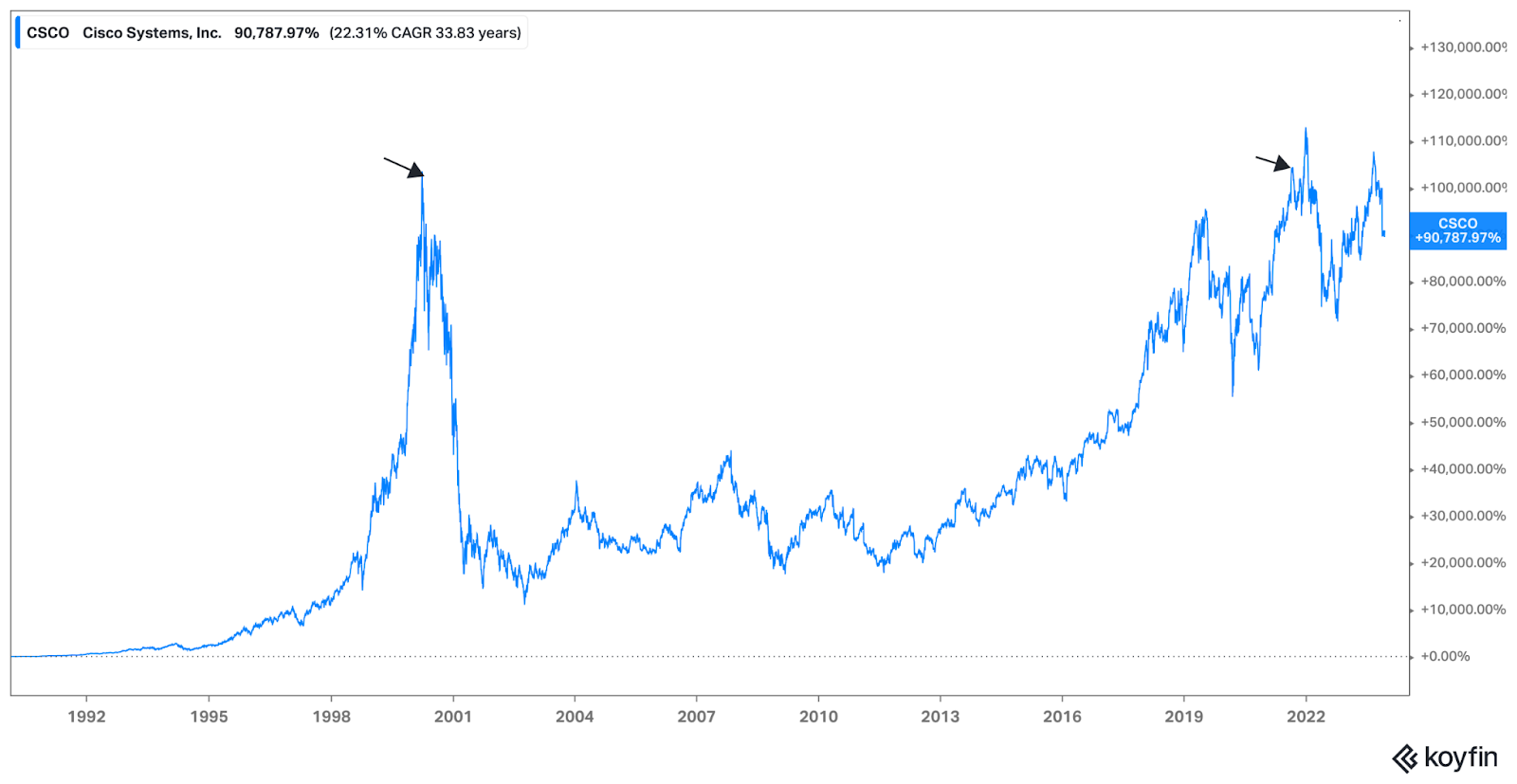

I have a family member who bought just a few stocks back in the late 1990’s, or early 2000’s. One of those was Cisco (CSCO). And she just happened to buy it at or near the top. Take a look at what’s happened in the 20+ years since:

Yes, the stock has recovered, but it took somewhere around 21 years to do so. She was convinced the stock market was too risky and stopped investing. Can you blame her?

The point is not that she bought a bad company (on the contrary, the chart above shows that Cisco has been a great investment over the very long term), it’s that she bought it when everyone else was, and therefore the price was detached from the fundamentals of the business.

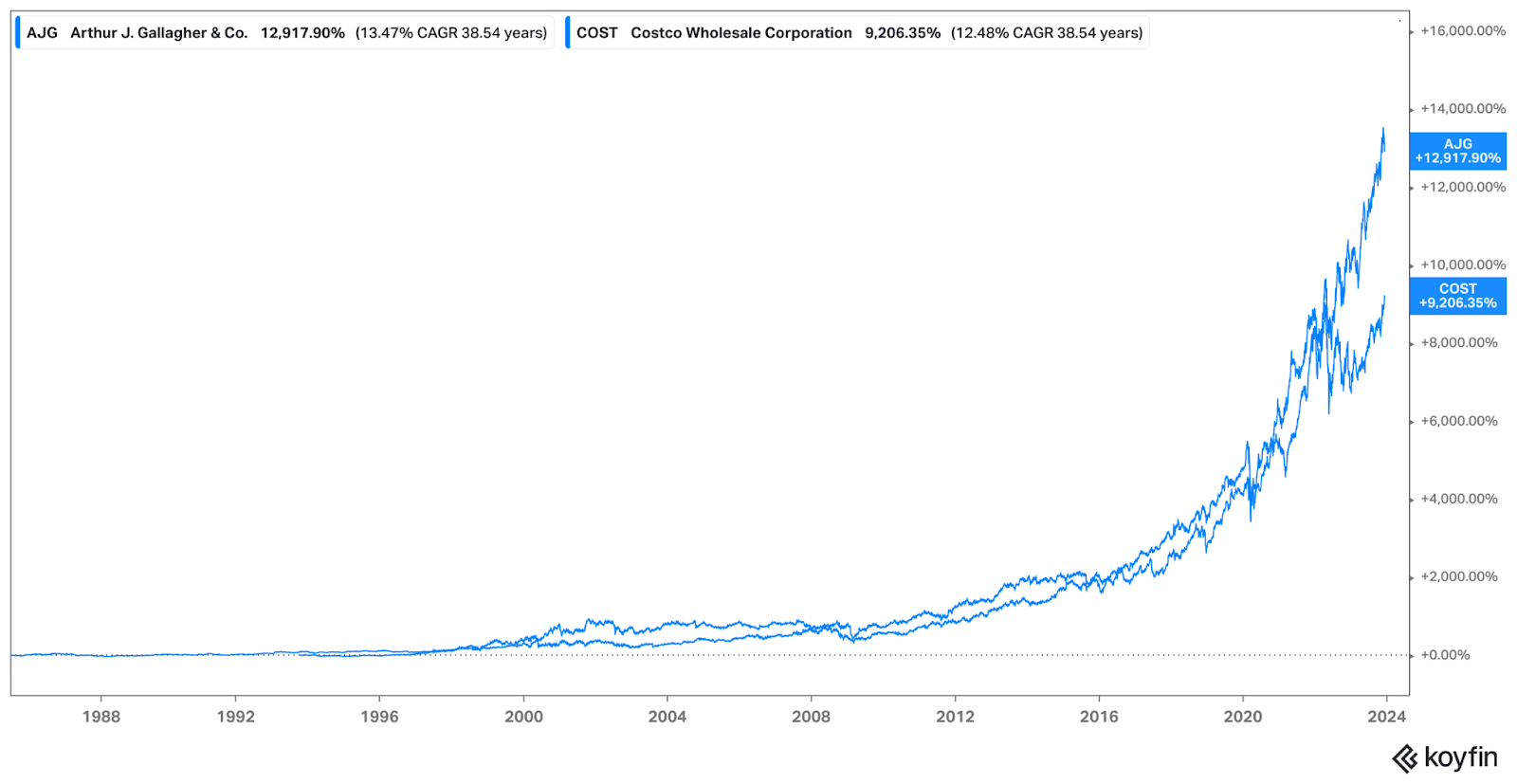

Now let’s look at one of the companies Tyler mentioned, Arthur J. Gallagher (AJG). During the episode, Tyler compared its return to that of Costco (COST) over the time since Costco came public.

Incredible. I believe a lot of this difference in performance is that fewer people have heard of one than the other. This is a nice example of how spending time looking into less well-known companies can yield better results.

If you’re reading this and you’re a stock picker, this is something I think is worth considering. I want to start fishing in these different ponds myself. I also may find myself relying on Tyler’s newsletter as well. It seems smart to use the subscription to better learn how to identify these kinds of companies.

I’ll still buy well-known stocks too. But I’m thinking that it might be wise to dedicate a portion of my portfolio to these “misfit” stocks. Especially at a time when it feels like all the well-known stocks I follow are becoming more and more expensive.

Jeff

Jason’s Random Words

Tyler and I have known each other for over a decade, both as colleagues and as friends. I’ve known about Misfit Alpha since before he launched it, and the research project that led to its creation.

I think one of the reasons why Tyler and I are close and work well together is that I have a little bit of “misfit” in me as well. I own my share of well-known giants like Nvidia (NVDA), and a well-followed winner like MercadoLibre (MELI) is my largest holding, both in total size and dollars invested, but I have also been fortunate to be exposed to — and occasionally find on my own — a lot of misfit-ish stocks in my career.

Axos Financial (AX) is a good example. Formerly known as Bank of the Internet, Axos shares have earned almost 2,700% in gains since Greg Garrabrants became CEO in 2007. That’s an incredible 22.8% CAGR, more than double the S&P 500 over the same period.

It’s also 8.5X the returns of Bank of America (BAC) and 7X JPMorgan Chase (JPM) over the same period, and within shouting distance of the 3,000% in gains Amazon (AMZN) investors have earned in that period. And it’s outperformed those bigger peers for good reason. As a smaller bank it’s been able to grow assets more quickly, and under Garrabrants, it has done so very profitable, and without taking on the sort of risk that always comes home to roost eventually.

Once again starting from the beginning of Garrabrants’ tenure as CEO, Axos has consistently generated higher returns on both assets and equity than its bigger peers. That’s created immense value and returns for shareholders.

Here’s where it’s still very much in the Misfit mold: With a market cap that’s still shy of $3 billion, it’s 1/20th the size of America’s biggest bank, and only six Wall Street firms even follow it, compared to more than 20 for Morgan, and over 30 following BofA. Even Tyler’s much-lauded Arthur J. Gallagher has 18 analysts following it.

Kinsale Capital (KNSL) is another example, and one that has so-far escaped Tyler’s notice because it hasn’t been around long enough to show up on his screeners. If you found our podcast or newsletter through our association with The Motley Fool, you may be familiar with Kinsale, making it seem popular. But I can tell you that broadly, it definitely fits the Misfit bill. Massive winner. Industry-leading metrics. Carved out a niche that it knows incredibly well and does better than its competitors. Showing no interest in deviating from what it does well. Far less

And since it’s mid-2016 IPO, shares are up 1,750%. That means the stock price has, on average, gained almost 49% a year since it went public. founder and CEO Michael Kehoe is doing it by building an insurance company focused on insuring the oddball stuff (called “excess and surplus) that most large property and casualty insurers don’t really want to deal with because they don’t scale up enough to be worth the effort. Exactly the sort of place where you’d expect to find companies that dominate a niche and generate wonderful returns for many, many years.

The point isn’t to rush out and buy shares of Axos (though it remains one of my favorite underappreciated small U.S. banks) or Kinsale (man, that stock is crazy expensive). It’s to point out that there are plenty of winning stocks out there that aren’t household names. And a lot of them have been winners for a very long time, and are built to keep being winners.

Jason

Reply